Most employers approach their health plan the same way every year. Renewal comes around, they review the numbers, make some adjustments, and move on. It is a familiar cycle and for many companies it has become routine enough that nobody questions whether there is a better way.

There is.

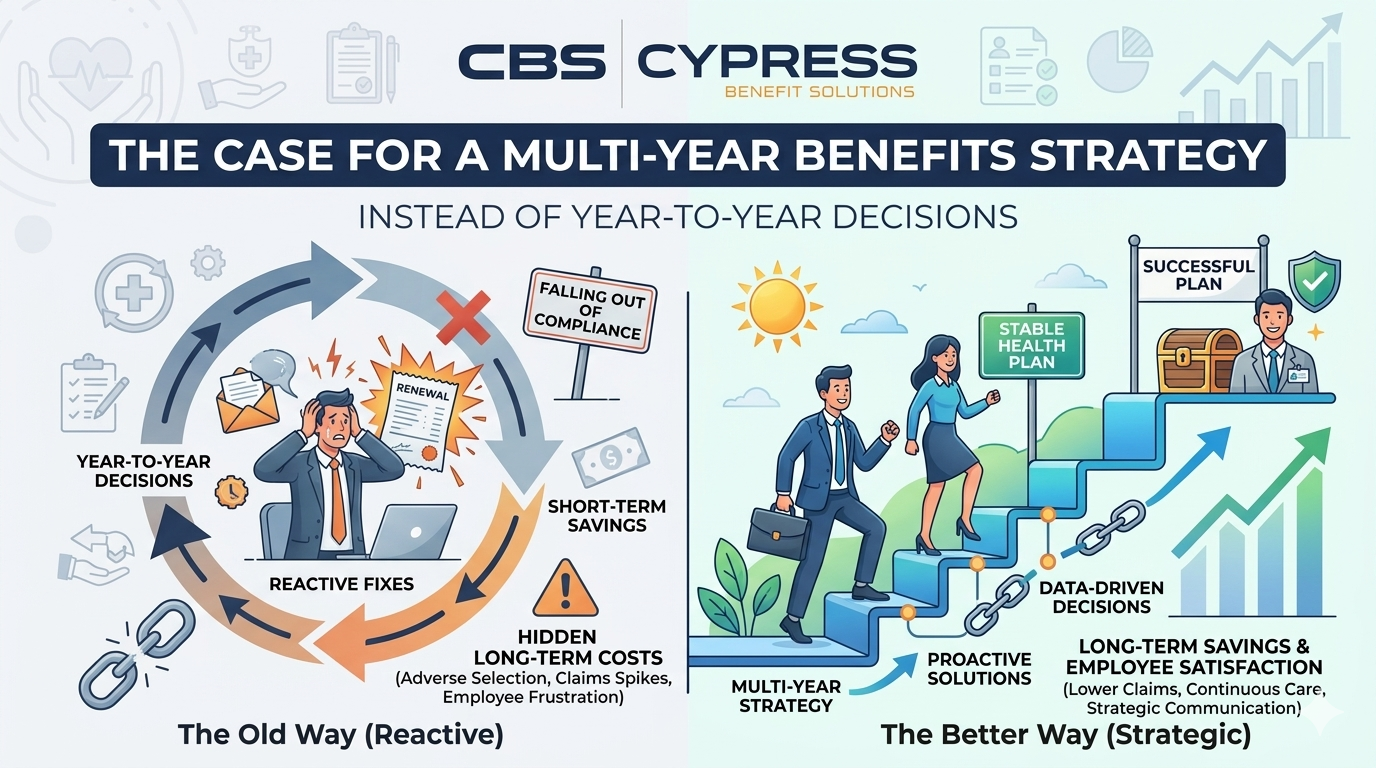

Employers who consistently manage their benefits costs effectively and maintain strong employee satisfaction with their coverage are rarely doing it by reacting well to each renewal. They are operating with a multi-year strategy, a coordinated plan that looks beyond the current renewal cycle and makes decisions with a longer time horizon in mind.

This post makes the case for why that approach produces better outcomes and what it actually looks like in practice.

Why Year-to-Year Decision Making Falls Short

When benefits decisions are made one year at a time, the natural tendency is to focus on the most immediate problem in front of you. If the renewal came in high, you look for ways to reduce the premium. If employees complained about cost sharing last year, you adjust the deductible. If a competitor added a new benefit, you consider adding it too.

Each of these responses might be reasonable in isolation. The problem is that they are reactive. They are solving last year’s problem rather than building toward a long-term outcome. And because benefits decisions have consequences that compound over time, reactive management tends to produce results that are harder to course-correct the longer they go on.

There are several specific ways that year-to-year thinking tends to cost employers more over time.

Structural Problems Go Unaddressed

Some cost drivers in a health plan are not going to be solved by a plan design tweak at renewal. If your plan is attracting adverse selection, if your pharmacy benefit is poorly structured, or if your contribution strategy is creating unintended consequences for workforce demographics, these are structural issues that require deliberate, multi-year solutions. Reacting to symptoms at renewal time rarely addresses root causes.

Short-Term Savings Create Long-Term Costs

Raising deductibles and shifting cost to employees is one of the most common renewal responses. It reduces the employer’s premium contribution in the short term, but it also discourages employees from seeking care. As we have covered in previous posts, employees who avoid care tend to generate higher claims costs down the road. The short-term savings often come at the expense of higher long-term spend.

Carrier and Plan Changes Disrupt Continuity

When employers switch carriers or dramatically restructure their plan design every year or two in pursuit of lower premiums, they lose continuity. Employees lose familiarity with their coverage. Claims history gets interrupted. The employer loses the data continuity needed to identify trends and make informed decisions. Stability has value that is easy to underestimate.

Reactive Decisions Miss Strategic Opportunities

Some of the most effective cost management tools available to employers, such as alternative funding arrangements, direct primary care partnerships, reference-based pricing, and population health programs, require planning horizons longer than a single renewal cycle. Employers who are always focused on the next renewal never get around to evaluating whether these approaches might produce better long-term results.

What a Multi-Year Benefits Strategy Actually Looks Like

A multi-year strategy is not a complicated document or a rigid five-year plan. It is a shared understanding between you and your benefits advisor about where you are today, where you want to be, and what steps will get you there over a defined time horizon. Here is what that typically involves.

A Clear Baseline Assessment

Before you can build a strategy, you need an honest picture of where you stand. This means understanding your current cost per employee, how that compares to benchmarks for your industry and region, what is driving your claims experience, how your employees feel about their current coverage, and whether your contribution strategy is achieving the outcomes you intended. This baseline becomes the foundation everything else is built on.

Defined Goals With a Time Horizon

A strategy requires goals. For most employers those goals sit in a few categories: managing cost growth to a sustainable rate, maintaining or improving the quality of coverage employees receive, supporting workforce attraction and retention, and ensuring compliance with evolving regulatory requirements. Defining these goals explicitly, and agreeing on what success looks like over a two or three year period, gives every subsequent decision a clear frame of reference.

A Funding Structure Conversation

One of the most significant decisions in any multi-year benefits strategy is whether the current funding structure, typically fully insured, is still the right fit. For employers who have historically been on fully insured plans, a multi-year strategy creates the opportunity to evaluate whether a level-funded or self-funded arrangement might produce better long-term outcomes given the size and health profile of their workforce. This is not the right move for every employer, but it is a conversation that should happen within a strategic framework rather than being dismissed or pursued reactively.

Annual Plan Reviews Tied to Strategy, Not Just Renewal

In a multi-year strategy, the annual renewal review becomes a checkpoint against the larger plan rather than a standalone event. The questions change. Instead of asking only what the renewal number is and how to offset it, you are also asking whether you are on track toward your goals, whether the data from the past year is telling you something new, and whether any adjustments to the strategy are warranted. This produces more thoughtful decisions and reduces the likelihood of making changes that solve the immediate problem while creating new ones.

Communication as a Strategic Component

Benefits communication is often treated as an afterthought, something to handle during open enrollment. In a multi-year strategy, communication is a deliberate component of the plan. If you are trying to improve preventive care utilization, that requires sustained communication throughout the year. If you are introducing a new plan option or a different funding structure, employees need time and context to understand the change. Treating communication as part of the strategy rather than an annual task produces meaningfully better outcomes.

The Cost Savings Case

The business case for a multi-year strategy is straightforward. Employers who operate strategically tend to see more stable cost growth over time because they are addressing root causes rather than symptoms. They are more likely to have the data visibility needed to make informed decisions. They are better positioned to evaluate alternative funding arrangements that can produce real savings. And they avoid the compounding costs that come from repeated short-term fixes.

None of this means costs never go up. Healthcare cost trend is real and no strategy eliminates it entirely. But there is a meaningful difference between an employer whose costs track the national trend and one whose costs consistently outpace it. Multi-year strategic management tends to produce the former.

There is also a retention argument. Employers who think strategically about their benefits tend to have more coherent, competitive packages. They are not making reactive cuts that erode employee confidence in their coverage. They are building toward something, and employees notice.

How Cypress Benefit Solutions Approaches This

At Cypress Benefit Solutions, we do not think our job is to shop your renewal once a year and hand you a quote. Our job is to be a strategic partner who helps you build and execute a benefits strategy that produces real results over time.

That means starting with a thorough assessment of where your plan stands today, helping you define what you are trying to accomplish over the next several years, and then working with you throughout the year, not just at renewal, to make sure the strategy is on track. When market conditions change, when your workforce evolves, or when new tools and programs become available, we bring those conversations to you proactively rather than waiting for you to ask.

If your current approach to benefits feels like a series of reactions rather than a coherent plan, that is worth changing. A multi-year strategy is not complicated to build, but it does require a benefits partner who is invested in your long-term outcomes. That is exactly the kind of relationship we are looking to build with every employer we work with.

If you would like to talk through what a strategic benefits review might look like for your company, we would welcome the conversation. Reach out anytime.