Mental health parity is one of those compliance topics that most employers have heard of but far fewer actually understand. The result is that a significant number of health plans are currently out of compliance with federal law, and the employers sponsoring those plans may not know it until a regulator comes looking.

2026 is a year when that risk is particularly elevated. Federal enforcement of the Mental Health Parity and Addiction Equity Act, commonly known as MHPAEA, has intensified significantly, and the rules employers are expected to follow have become more demanding. This post explains what MHPAEA requires, what has changed, where plans most commonly fall short, and what employers should be doing right now.

What Mental Health Parity Actually Means

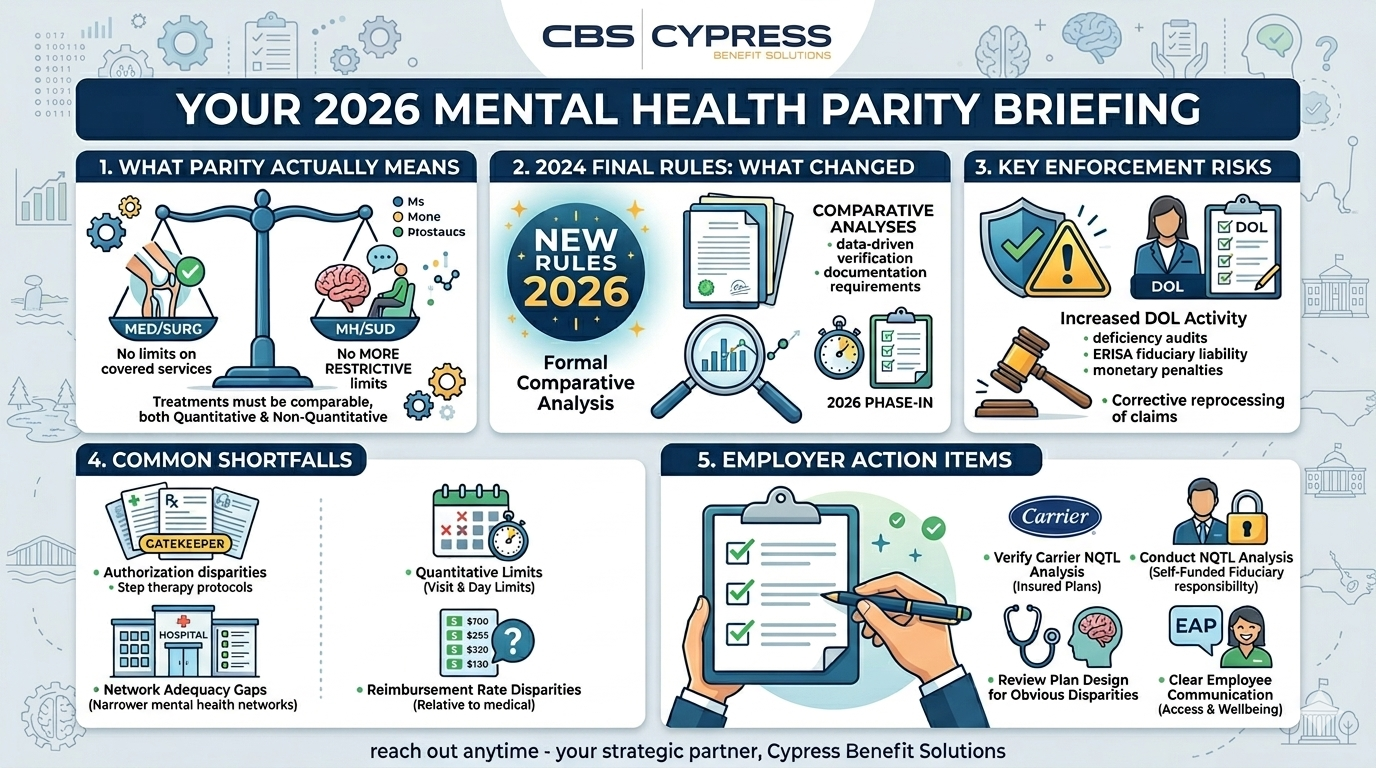

MHPAEA is a federal law originally passed in 2008 that requires group health plans offering mental health and substance use disorder benefits to provide those benefits on terms no more restrictive than the plan’s medical and surgical benefits. The core principle is straightforward: if your health plan covers a knee replacement without a visit limit, it cannot cap inpatient psychiatric care at 30 days. If your plan does not require prior authorization for an outpatient specialist visit, it cannot require prior authorization for an outpatient therapy appointment of equivalent intensity.

Parity applies across two dimensions. Quantitative treatment limitations are numerical restrictions like visit caps, day limits, and dollar limits. Non-quantitative treatment limitations, commonly called NQTLs, are non-numerical restrictions such as prior authorization requirements, step therapy protocols, network admission standards, reimbursement rates, and utilization management criteria. Both types must be applied to mental health benefits in a way that is no more restrictive than how they are applied to comparable medical and surgical benefits.

Importantly, MHPAEA does not require employers to offer mental health benefits at all. But if a plan covers mental health or substance use disorder conditions, it must cover them in parity with everything else the plan covers.

What Changed With the 2024 Final Rules

In September 2024, the U.S. Departments of Labor, Health and Human Services, and Treasury released significant new final rules implementing MHPAEA. Most provisions took effect for plan years beginning January 1, 2025, with additional requirements phasing in for the 2026 plan year.

The most important change is the elevated requirement around comparative analyses. Plans are now required to conduct and document a formal comparative analysis of their non-quantitative treatment limitations, demonstrating with data that mental health benefits are truly equivalent to medical and surgical benefits not just in how they are written on paper but in how they actually function in practice. Regulators have made clear that listing mental health benefits in a summary plan description is not the same as meaningfully covering them, and the new rules give federal agencies additional analytical tools to tell the difference.

The 2024 rules also codify a meaningful benefits standard, which requires that plans provide genuine access to mental health and substance use disorder care, not nominal coverage that is structured in a way that makes it effectively inaccessible. Network adequacy is a specific focus area, as mental health provider networks have historically been narrower and reimbursement rates for mental health providers have historically been lower than for medical providers. Under the current rules, those disparities are not just market problems. They are potential parity violations.

Why Enforcement Is a Real and Immediate Risk

MHPAEA has been on the books since 2008, but enforcement has historically been inconsistent. That has changed meaningfully in recent years. The Department of Labor has significantly increased its enforcement activity, and the agencies now have more analytical sophistication and more legal authority to pursue violations than at any point in the law’s history.

The DOL’s own enforcement reports have consistently found that the majority of plans reviewed had compliance deficiencies. Enforcement actions can result in required plan design changes, corrective reprocessing of denied claims, civil monetary penalties, and in cases involving serious violations, individual fiduciary liability under ERISA. Plans that have never conducted a formal NQTL comparative analysis are at substantially higher risk, as are plans that conducted one under older standards but have not updated it to reflect the current rules.

For employers, the exposure is real and the window to get ahead of it is narrow. Employers who identify and address deficiencies proactively are in a meaningfully better position than those who wait for a regulatory inquiry.

Where Plans Most Commonly Fall Short

Based on DOL enforcement patterns and the areas explicitly flagged in the 2024 final rules, the most common parity violations fall into a few recognizable categories.

Prior Authorization Disparities

Requiring prior authorization for mental health or substance use disorder services while not requiring it for comparable medical services is one of the most frequently cited violations. A plan that requires pre-authorization for outpatient therapy but not for outpatient specialist visits of equivalent intensity is not in compliance. The comparison has to be made at the same level of care and benefit classification, and the criteria used to make authorization decisions must be equally rigorous in both directions.

Visit and Day Limits

Capping mental health inpatient days or outpatient therapy visits at a level that has no equivalent cap on medical services is a quantitative treatment limitation violation. This is one of the more straightforward areas to identify, but it remains common in plans that have not been reviewed against current standards.

Network Adequacy Gaps

Mental health provider networks are frequently narrower than medical networks, which means employees seeking mental health care are more likely to end up out of network and facing higher costs. Under the 2024 rules, plans are required to collect and analyze data on in-network utilization rates, out-of-network claim rates, and provider reimbursement rates relative to medical and surgical providers. If the data shows a material disparity, the plan must take action to address it. Network adequacy is one of the highest-priority areas for federal regulators in 2026.

Reimbursement Rate Disparities

Historically lower reimbursement rates for mental health providers have contributed to network shortages and reduced employee access to in-network care. Plans are now expected to evaluate whether their reimbursement rate structure for mental health providers is comparable to what medical and surgical providers receive for equivalent services. If it is not, that disparity is a parity issue under the current rules.

Inaccurate Provider Directories

Regulators are increasingly examining whether plan provider directories accurately reflect which mental health providers are accepting new patients, actively participating in the network, and offering timely appointments. A directory that lists many providers but in practice makes it difficult for employees to find one who is available and accepting new patients is not meeting the access standard the law requires.

What Employers Should Do Right Now

The compliance landscape around MHPAEA is more demanding than it has ever been, but it is also more navigable for employers who engage with it proactively. Here is where to focus.

Confirm Your Carrier Has Conducted a Current Comparative Analysis

For employers on fully insured plans, the primary responsibility for conducting the NQTL comparative analysis rests with the carrier. But employers retain a responsibility to review and sign off on that analysis, not simply accept it passively. Ask your carrier or benefits administrator whether a current comparative analysis has been completed, whether it reflects the 2024 final rules, and whether there are any identified deficiencies and how they are being addressed.

Understand Your Obligations as a Plan Sponsor

For self-funded employers, the fiduciary responsibility for parity compliance rests more directly with the plan sponsor. If your plan is self-funded and you have not engaged a qualified advisor to conduct or review a formal comparative analysis under current standards, that is a priority item. The documentation requirements are specific and the exposure for non-compliance is meaningful.

Review Your Plan Design for Obvious Disparities

Even without a formal comparative analysis, a review of your plan’s treatment limitations, prior authorization requirements, and network structure can surface obvious areas of concern. If your plan imposes visit limits on mental health services that have no equivalent on medical services, or requires prior authorization for mental health care that is not required for comparable medical care, those are issues worth addressing before a regulator identifies them first.

Communicate Clearly With Employees About Their Mental Health Benefits

Beyond the compliance dimension, clear employee communication about mental health benefits matters for utilization and wellbeing. Employees who do not know what their plan covers, how to find an in-network mental health provider, or how to access their EAP are less likely to seek care when they need it. Improving that communication is a worthwhile investment regardless of where your plan stands on technical compliance.

A Note on the Current Regulatory Environment

It is worth noting that as of early 2026, the updated 2024 final rules are operating under a non-enforcement policy from the current administration for certain provisions. However, the 2013 MHPAEA regulations remain the controlling standard and the DOL has indicated it continues to enforce existing parity requirements. Employers should not interpret the non-enforcement policy on the newer provisions as a signal that parity compliance is less important. The enforcement environment remains active and the underlying law has not changed.

How Cypress Benefit Solutions Can Help

Mental health parity compliance is an area where the complexity of the requirements and the pace of regulatory change make working with a knowledgeable benefits advisor genuinely valuable. Understanding what your plan’s comparative analysis covers, whether your carrier’s analysis meets current standards, and what your specific obligations are as a plan sponsor are questions that deserve thoughtful answers.

At Cypress Benefit Solutions, we help employers navigate compliance requirements like MHPAEA as part of our broader benefits advisory work. If you are not sure where your plan stands on mental health parity, or if this topic has not come up in your benefits conversations recently, that is a conversation worth having. Reach out anytime and we would be glad to help you think through it.