If you have been offering health insurance for any length of time, you have almost certainly been doing it the same way: you pay a premium to an insurance carrier, the carrier covers your employees’ claims, and the premium goes up every year whether your employees used a lot of care or very little. That model is called fully insured, and for many employers it is simply the way benefits have always worked.

But there is another way. A growing number of employers, including many in the 50 to 200 employee range, are moving away from fully insured plans and toward self-funded arrangements that give them more control over their costs, more transparency into their claims data, and the real possibility of meaningful savings when their workforce stays healthy.

This post is a plain-language introduction to self-funding. What it is, how it works, what it costs, who it is right for, and what the risks actually look like in practice. If you have heard the term but never had it explained clearly, this is a good place to start.

What Fully Insured Really Means

Before explaining self-funding it helps to be clear about what fully insured actually means, because most employers accept it without fully understanding the financial structure behind it.

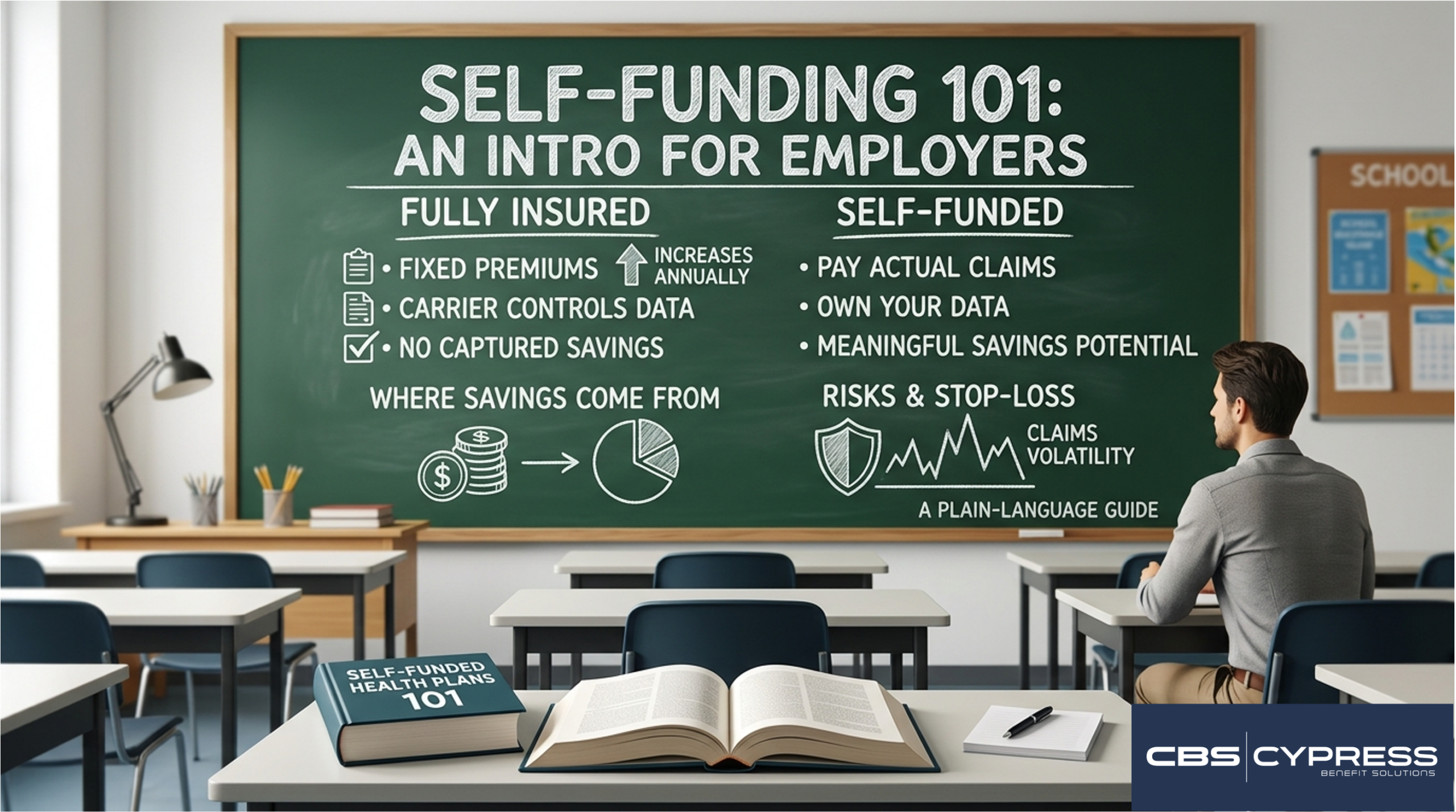

When you buy a fully insured health plan, you are paying the carrier a fixed monthly premium for each covered employee and dependent. In exchange, the carrier agrees to pay all covered claims regardless of how high they run. If your employees have a terrible claims year, the carrier absorbs the loss. If they have a great year with minimal claims, the carrier keeps the surplus.

That risk transfer has a price. Embedded in every fully insured premium is the carrier’s profit margin, their administrative costs, their risk charge for taking on the uncertainty of your claims, and a contribution to their reserves. Industry estimates put the non-claims portion of a fully insured premium at somewhere between 20% and 30% of the total premium dollar depending on the carrier and the group size. That means for every dollar you spend on health insurance, as much as 25 to 30 cents may never touch an actual medical claim.

In a good claims year, that money is simply gone. You have no mechanism to capture any of it back.

How Self-Funding Works

In a self-funded arrangement, the employer takes on the financial responsibility for paying employee health claims directly rather than transferring that risk to a carrier in exchange for a fixed premium. Instead of paying a bundled premium, the employer pays for three distinct components each month.

Claims Costs

The employer pays actual claims as they are incurred by covered employees and dependents. In a good month, this number is low. In a month with a large claim, it is higher. Over the course of a plan year, the employer’s total claims cost reflects what their specific employee population actually used, not what a carrier estimated they might use when setting the premium.

Stop-Loss Insurance

This is the component that makes self-funding financially manageable for smaller employers. Stop-loss insurance is a separate insurance policy that protects the employer from catastrophic claims. It comes in two forms. Specific stop-loss, sometimes called individual stop-loss, reimburses the employer when any single employee’s claims exceed a defined threshold in a plan year, typically somewhere between $25,000 and $150,000 depending on how the coverage is structured. Aggregate stop-loss provides a second layer of protection by capping the employer’s total claims liability for the entire plan at a defined percentage of expected claims, usually around 125%. Together these two coverages mean that while the employer is technically paying claims directly, their financial exposure is bounded and predictable.

Administrative Fees

Self-funded plans require a third-party administrator, commonly called a TPA, to handle claims processing, member services, network access, and plan administration. The TPA charges a per-employee per-month fee for these services. Most self-funded employers also continue to access a carrier’s provider network through a network access arrangement, which typically carries its own fee. The combination of TPA fees and network access costs is generally significantly lower than the administrative and profit load embedded in a fully insured premium.

Where the Savings Come From

The cost savings potential in self-funding comes from several places, and understanding each one helps explain why employers with healthy workforces tend to benefit most.

Eliminating the Carrier’s Risk Charge and Profit Margin

As noted above, a meaningful portion of a fully insured premium goes to the carrier’s profit and risk reserves rather than to paying claims. In a self-funded arrangement, that money stays with the employer. If claims run below the carrier’s expectation, the employer captures the difference rather than the carrier. Over multiple years in a self-funded arrangement, employers with favorable claims experience can generate savings that would simply not be available under a fully insured model.

State Premium Tax Savings

Fully insured premiums are subject to state premium taxes, which typically run between 2% and 3% of premium depending on the state. Self-funded plans are governed by federal ERISA law rather than state insurance regulations, which means they are not subject to state premium taxes or many state-mandated benefit requirements. For an employer spending several hundred thousand dollars a year on health benefits, the tax savings alone can be meaningful.

Access to Your Own Claims Data

One of the most underappreciated advantages of self-funding is data access. On a fully insured plan, your claims data belongs to the carrier. You may receive summary reports, but the detailed information needed to understand what is driving your costs is typically not available to you. On a self-funded plan, you own your claims data. That means you can see exactly what services are being used, identify cost drivers, evaluate the effectiveness of specific benefits, and make data-informed decisions about plan design. For employers who want to actively manage their health plan rather than simply renew it each year, this visibility is genuinely transformative.

Plan Design Flexibility

Self-funded plans are not subject to many of the state benefit mandates that apply to fully insured plans. This gives employers more flexibility to design a plan that fits their specific workforce rather than accepting a standardized product. It also makes it easier to implement targeted cost management strategies, such as value-based plan designs that waive cost sharing for high-value preventive services or direct primary care arrangements that provide employees with enhanced primary care access at predictable cost.

What the Risks Actually Look Like

The most common concern employers raise about self-funding is cash flow volatility. On a fully insured plan, your monthly cost is predictable. On a self-funded plan, your claims cost varies month to month, and a bad month can feel alarming even when the annual experience is favorable.

This is a legitimate concern and one worth taking seriously, but it is also one that stop-loss insurance largely addresses. With properly structured specific and aggregate stop-loss coverage in place, the employer’s worst-case scenario in any given plan year is known and bounded before the year begins. The remaining variability is real but manageable for most employers who have adequate cash reserves or access to a line of credit.

A second concern is the administrative complexity of self-funding relative to fully insured. This is also legitimate, though the practical burden on the employer is often less than anticipated. A good TPA handles the vast majority of day-to-day administration, and a knowledgeable benefits advisor can manage much of the oversight and strategic work. What self-funding does require is an employer who is willing to be more engaged with their health plan than a fully insured arrangement demands. For employers who want that engagement, it is an advantage. For those who want to be entirely hands-off, it may not be the right fit.

Is Self-Funding Right for Your Company?

Self-funding is not the right answer for every employer. But it deserves a serious look from a wider range of employers than currently consider it. Here are the factors that most influence whether a self-funded arrangement is likely to be a good fit.

Group Size

Self-funding has historically been associated with large employers, but the availability of stop-loss insurance and increasingly competitive TPA pricing has made it viable for groups as small as 25 to 50 employees in many markets. Employers in the 50 to 200 employee range are a natural fit for evaluation, particularly those with stable workforces and relatively favorable claims history. The larger the group, the more predictable the claims experience tends to be, which generally makes self-funding more financially stable.

Workforce Health Profile

Employers with younger, healthier workforces tend to benefit most from self-funding because their actual claims costs are likely to be lower than what a carrier prices into a fully insured premium. Employers with older workforces or known high-cost claimants can still self-fund effectively, but the stop-loss structure and expected claims assumptions need to be modeled carefully. A thorough analysis of your current claims experience and workforce demographics is essential before making this decision.

Cash Flow and Financial Stability

Self-funding requires the employer to have sufficient cash flow or credit access to pay claims as they are incurred. While stop-loss insurance caps the worst-case exposure, the timing of large claims can create short-term cash flow demands. Employers with tight cash flow or limited reserves should discuss this dimension carefully with their advisor before moving forward.

Appetite for Engagement

Self-funded employers who get the most out of the arrangement are those who are willing to review their claims data regularly, make plan design decisions based on what the data tells them, and work actively with their benefits advisor to manage their plan as the strategic asset it is. Employers who want a fully passive relationship with their health plan may find the fully insured model more comfortable, even if it costs more.

How Cypress Benefit Solutions Approaches This Conversation

Self-funding is one of the areas where the value of working with an independent, carrier-agnostic benefits advisor is most apparent. Many brokers steer employers away from self-funded arrangements because they are more complex to implement and manage than simply renewing a fully insured plan. At Cypress Benefit Solutions, we believe every employer in the right size range deserves a clear and honest analysis of whether self-funding makes sense for their specific situation, without a predetermined answer.

That analysis starts with your current claims experience, your workforce demographics, your cash flow position, and your appetite for engagement with your health plan. From there we can model what a self-funded arrangement would have looked like historically and what a reasonable range of outcomes might look like going forward. That modeling does not always point toward self-funding, but it always produces a more informed conversation than one that never happens at all.

If you have never had this conversation with your benefits advisor, or if you have been told self-funding is not for companies your size without ever seeing the analysis behind that conclusion, we would welcome the opportunity to take a fresh look. Reach out anytime.