If you have been watching your health plan costs climb over the past few years and wondering whether things are going to level off anytime soon, the short answer is not yet. The data coming out of major employer health surveys for 2026 tells a consistent story: healthcare costs are rising at the fastest pace in over a decade, and the factors driving those increases are not temporary.

This post is designed to give you a clear picture of what is actually happening in the market, why it is happening, and what it means for employers who are heading into a renewal in the months ahead. Think of it as a market briefing from your benefits advisor rather than a surprise at renewal time.

The Numbers Every Employer Should Know

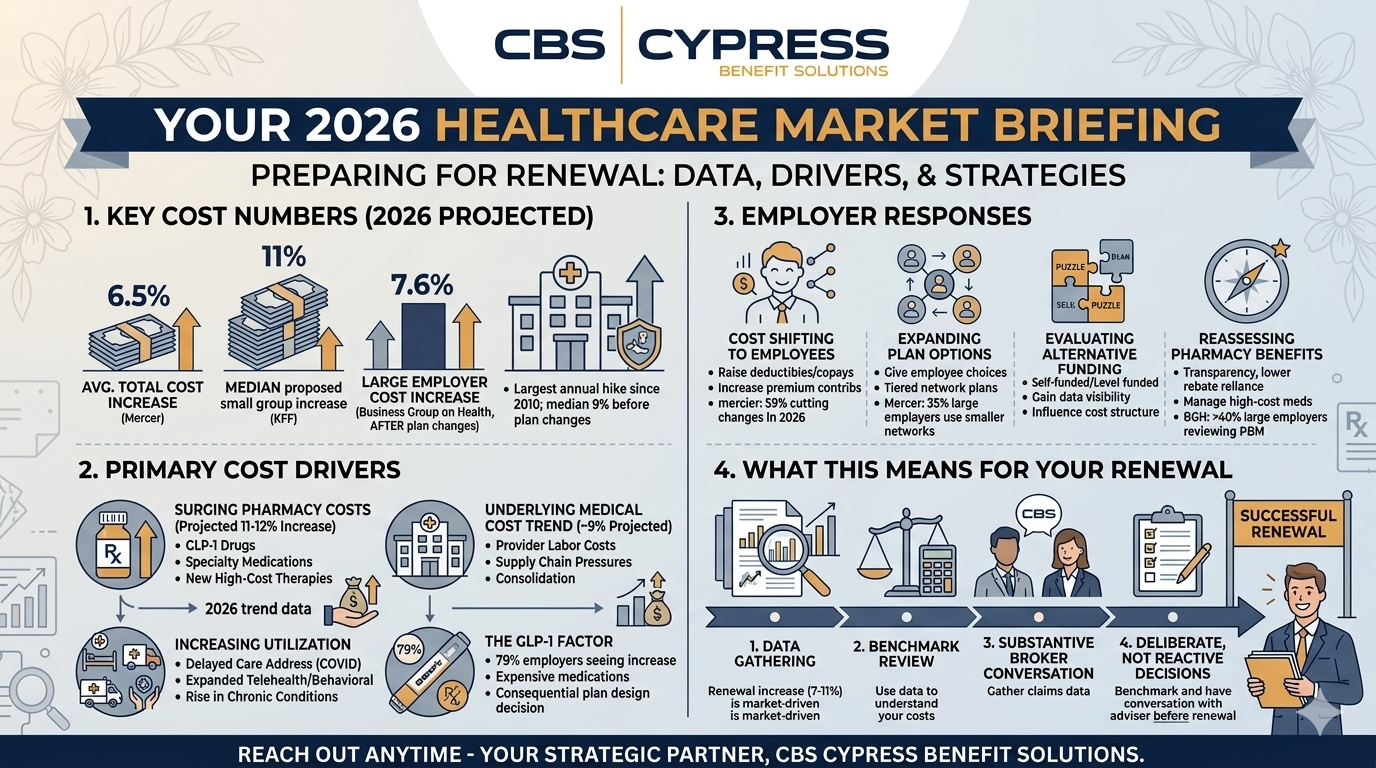

The scale of the current cost environment is worth understanding before getting into the causes. According to Mercer’s 2025 National Survey of Employer-Sponsored Health Plans, total health benefit cost per employee is projected to increase an average of 6.5% in 2026. That is the largest single-year increase since 2010 and represents a significant departure from the decade prior, when annual increases averaged closer to 3%.

Without plan design changes, that number would have been closer to 9%. Many employers are absorbing the difference by raising deductibles, increasing employee premium contributions, or both.

For small employers specifically, the picture is even more pointed. An analysis of small group insurance filings by the Peterson-KFF Health System Tracker found that the median proposed premium increase among small group insurers for 2026 is 11%, with some states seeing proposed increases considerably higher than that.

The Business Group on Health, whose survey covers large employers, puts the projected cost trend at a median of 9% before plan design adjustments, settling to around 7.6% after changes are made. On a compounded basis, health benefit costs in 2026 are expected to be roughly 62% higher than they were in 2017.

These are not outlier projections from a single source. They are broadly consistent findings across multiple credible research organizations, and they represent the environment your next renewal is being priced in.

What Is Actually Driving the Increases

Understanding the causes matters because the right response depends on which factors are most affecting your specific plan. There are several distinct cost drivers active in the current environment, and most employers are dealing with some combination of all of them.

Rising Healthcare Service Costs

The underlying cost of medical services continues to increase across the board. Hospitals, physician practices, and other providers are facing higher labor costs, supply chain pressures, and the ongoing effects of provider consolidation into larger health systems. Consolidation in particular has given providers increased leverage in negotiating reimbursement rates with insurers, and those higher rates flow directly into employer premiums. Insurers in their rate filings commonly estimate that the underlying medical cost trend for 2026 is running around 9%, meaning the cost of care itself is rising nearly 9% before any changes in how often people use it.

Surging Pharmacy Costs

Pharmacy spend has become one of the most significant and fastest-growing components of employer health plans. According to the Business Group on Health, pharmacy expenses accounted for roughly 24% of total employer healthcare spend in 2024, and employers are projecting an 11% to 12% increase in pharmacy costs heading into 2026. Specialty medications, the rising use of GLP-1 drugs for weight management, and a pipeline of new high-cost therapies are the primary contributors. This is a cost category that plan design adjustments alone cannot solve, and it is driving serious conversations among employers about pharmacy benefit structure and PBM relationships.

Increasing Utilization

It is not just the price of healthcare that is rising. People are using more of it. Utilization rates across a range of health services have been climbing over the past two years. Some of this reflects the delayed care that built up during the COVID-19 pandemic finally being addressed. Some of it reflects the expansion of telehealth and behavioral health access, which has made care more accessible and brought more people into the system who might not have sought care previously. Rising rates of chronic conditions, cancer diagnoses, and mental health utilization are all contributing. More use of the healthcare system, even when driven by legitimate need, translates directly into higher costs for the plans that cover it.

The GLP-1 Factor

As covered in a previous post, GLP-1 medications like Ozempic, Wegovy, and Zepbound are a growing cost driver that deserves its own mention. According to the Business Group on Health survey, 79% of employers are currently seeing an increase in the utilization of obesity medications among their covered population, and an additional 15% expect to see increases in the future. These are expensive medications, and the question of how to cover them or not cover them is one of the more consequential plan design decisions employers are navigating right now.

How Employers Are Responding

Given the scale of the cost environment, it is worth understanding how other employers are approaching the situation. The survey data is useful here because it shows not just what is happening but what the range of responses looks like.

Cost Shifting to Employees

The most common response remains raising deductibles, copays, and employee premium contributions. According to Mercer, 59% of employers plan to make cost-cutting changes to their plans in 2026, up from 44% in 2024. This is an understandable short-term response but one that carries risks. As we have discussed previously, higher employee cost sharing tends to discourage care-seeking, which can drive up longer-term costs when conditions go unmanaged and escalate.

Evaluating Alternative Funding Structures

More employers are taking a serious look at self-funded and level-funded arrangements as a way to gain more control over their cost structure. When an employer is fully insured, they have limited visibility into what is driving their costs and limited ability to influence it. Alternative funding structures give employers access to their own claims data, the ability to design more targeted solutions, and the potential to capture savings when claims run favorably. This is not the right fit for every employer, but interest in these models is growing meaningfully.

Reassessing Pharmacy Benefit Arrangements

With pharmacy costs representing nearly a quarter of total health spend, employers are paying closer attention to how their pharmacy benefit is structured. More than 40% of large employers surveyed by the Business Group on Health said they are either changing their pharmacy benefit manager or conducting a formal review. The focus is on greater transparency, less reliance on rebate arrangements that can obscure true drug costs, and better tools for managing high-cost medications.

Expanding Plan Options

Rather than making one-size-fits-all changes that affect every employee the same way, some employers are adding plan options that give employees more choices based on their individual health needs and financial situations. Tiered network plans, high-deductible options paired with HSAs, and plans that direct employees to high-quality lower-cost providers are all seeing increased adoption. Mercer’s data shows that 35% of large employers now offer at least one plan that uses a smaller, higher-performing provider network as a cost management tool.

What This Means for Your Renewal Conversation

The environment described above is the context in which your next renewal is being built. Whether you are heading into a July renewal in the next few months or a January renewal later in the year, there are a few things worth taking into your planning conversations.

First, a renewal increase in the range of 7% to 11% is not necessarily a sign that your plan is performing poorly. It may simply reflect the market environment your carrier is operating in. Understanding the difference between market-driven trend and plan-specific performance is important before deciding how to respond.

Second, the employers who are managing through this environment most effectively are not simply absorbing increases or shifting costs to employees. They are using data to understand what is driving their specific costs, evaluating whether their plan structure is still the right fit, and making deliberate decisions rather than reactive ones.

Third, the best time to have these conversations is before renewal pressure arrives, not during it. If your renewal is coming up in the next three to six months, now is the time to be gathering your claims data, reviewing your benchmarks, and having a substantive conversation with your benefits advisor about what options are available to you.

At Cypress Benefit Solutions, helping employers navigate exactly this kind of environment is the work we do every day. If you would like to talk through what the current cost trends mean for your specific plan and your upcoming renewal, we would welcome that conversation. Reach out anytime.