Most employers believe they offer a good benefits package. And most of the time, they are right in the sense that they are covering the basics and spending real money to do it. But there is a meaningful difference between a benefits package that exists and one that actually works, one that attracts the right people, supports employees when they need it most, and delivers value that justifies the investment.

This post walks through what a great employee benefits package actually looks like across each major category and gives you a practical self-assessment framework to evaluate whether yours is hitting the mark. By the end, you should have a clear picture of where your package is strong, where it has gaps, and where there may be opportunities to improve without necessarily spending more.

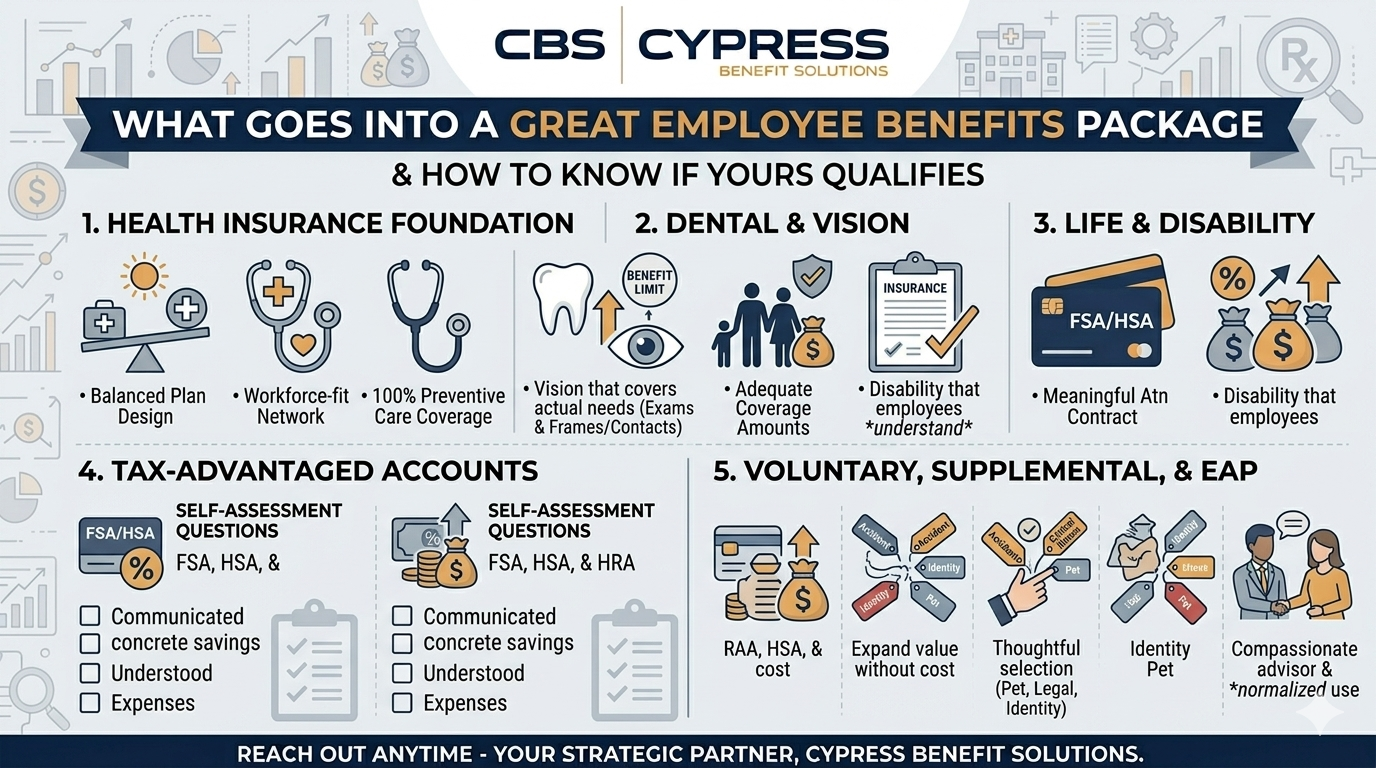

Start With the Foundation: Health Insurance

Health insurance is the centerpiece of nearly every employer benefits package and the benefit employees consistently rank as most important. Getting this right matters more than anything else on the list.

A strong health plan offering goes beyond simply having coverage in place. Here is what distinguishes a well-designed health plan from one that is just checking a box.

Plan Design That Balances Cost and Access

A great health plan gives employees meaningful access to care without creating financial barriers that discourage them from using it. Deductibles and out-of-pocket costs should be set thoughtfully, not simply maximized to reduce the premium. High deductibles save the employer money on the front end but can drive up long-term claims costs when employees delay or avoid care they need. The right design depends on your workforce demographics, wage levels, and utilization patterns, and it should be revisited regularly rather than left unchanged year after year.

A Network That Reflects Where Your Employees Actually Live and Work

A plan is only as useful as the providers in its network. Employees who cannot find their current doctor in-network, or who live in an area with limited network coverage, will either pay more for out-of-network care or go without it. Reviewing your network for fit with your actual workforce, not just your primary office location, is a step many employers skip and later regret.

Coverage for Preventive Care at No Cost

Most ACA-compliant plans cover preventive services including annual physicals, screenings, and vaccinations at 100% with no cost to the employee. Employers should confirm their plan covers these services correctly and make sure employees know about it. Preventive care utilization is one of the most effective long-term cost management tools available, and it only works if employees actually use it.

Self-Assessment Questions for Health Insurance

☐ Do we know what is driving our health plan cost increases each year?

☐ Is our deductible level appropriate for our employees’ financial situations?

☐ Have we confirmed our network still includes the providers our employees use most?

☐ Do employees know that preventive care is covered at no cost?

☐ Have we evaluated whether our current funding structure is still the right fit?

Dental and Vision: The Benefits Employees Notice

Dental and vision coverage sit just below health insurance in terms of how much employees value them and how often they use them. They are also two of the most common areas where employer coverage has not kept pace with actual costs.

Dental Coverage With Meaningful Maximums

Annual dental maximums that have not been updated in years often leave employees with significant out-of-pocket exposure on anything beyond routine cleanings and x-rays. A filling, a crown, or any orthodontic work can quickly exceed a $1,000 annual maximum that may have been set a decade ago. Reviewing your dental maximum against the actual cost of common procedures and considering whether an increase is warranted is a straightforward improvement that employees notice immediately.

Vision Coverage That Covers What Employees Actually Need

Vision plans vary significantly in what they cover and at what frequency. A plan that covers an eye exam every two years and a modest frame allowance is meaningfully different from one that covers annual exams and provides a reasonable allowance for lenses and frames or contact lenses. If your vision plan feels thin when you actually look at what it covers, it probably is.

Self-Assessment Questions for Dental and Vision

☐ When did we last review our dental annual maximum against current procedure costs?

☐ Does our vision plan cover annual exams or only every two years?

☐ Are employees satisfied with their dental and vision coverage or do we hear consistent complaints?

Life and Disability: The Safety Net Employees Rarely Think About Until They Need It

Life insurance and disability coverage are the benefits that employees tend not to think about until something goes wrong. When they do need them, however, the quality and adequacy of the coverage matters enormously.

Life Insurance That Provides Meaningful Protection

Employer-provided life insurance is often set at a flat amount or a single multiple of salary, and that amount may not have been revisited as salaries have grown. A benefit that was adequate three years ago may now fall short of what an employee’s family would need. Reviewing coverage amounts periodically and offering employees the ability to purchase supplemental coverage through voluntary options is a straightforward way to strengthen this benefit without a significant increase in employer cost.

Short-Term and Long-Term Disability That Employees Understand

Disability coverage is consistently one of the most misunderstood benefits in any package. Many employees have no idea what their plan covers, what the elimination period is, how long benefits last, or what percentage of their income is replaced. A package that includes disability coverage but never communicates it clearly is delivering far less value than it could. Strong packages not only have adequate coverage in place but make sure employees actually understand it.

Self-Assessment Questions for Life and Disability

☐ Have we reviewed our life insurance coverage amounts relative to current salary levels?

☐ Do employees know how to file a disability claim if they need to?

☐ Have employees been reminded to review and update their beneficiary designations recently?

☐ Do we offer voluntary supplemental life or disability options for employees who want more coverage?

Tax-Advantaged Accounts: The Underutilized Opportunity

Health Savings Accounts, Flexible Spending Accounts, and Health Reimbursement Arrangements are among the highest-value components of any benefits package from a pure financial return standpoint. They allow employees to pay for qualified medical expenses with pre-tax dollars, reducing their taxable income and the employer’s payroll tax obligation simultaneously. They are also consistently underutilized, typically because employees do not fully understand how they work.

A great benefits package not only offers these accounts where appropriate but actively communicates how to use them, what expenses qualify, and what the financial benefit actually is in concrete terms. An employee who understands that contributing $2,000 to an FSA saves them several hundred dollars in taxes is far more likely to participate than one who sees it as a complicated program they might not fully use.

Self-Assessment Questions for Tax-Advantaged Accounts

☐ Do we offer an HSA for employees enrolled in a high-deductible health plan?

☐ What percentage of eligible employees are contributing to our FSA or HSA?

☐ Have we communicated the tax savings benefit in concrete dollar terms to employees?

☐ Do employees know what expenses qualify for reimbursement?

Voluntary and Supplemental Benefits: Expanding Value Without Expanding Cost

Voluntary benefits are employer-sponsored options that employees elect and pay for themselves, typically at group rates that are more favorable than what they could access on their own. When structured well, they allow employers to meaningfully expand the perceived value of their benefits package without increasing their own cost.

Common voluntary options include accident coverage, critical illness insurance, hospital indemnity plans, identity protection, pet insurance, and legal services. None of these are right for every employer or every employee, but offering a thoughtful selection of voluntary options gives employees the ability to build a package that fits their personal situation rather than accepting a one-size-fits-all solution.

Self-Assessment Questions for Voluntary Benefits

☐ Have we reviewed what voluntary benefit options are available through our carrier or broker?

☐ Do employees know what voluntary options are available to them?

☐ Are there gaps in our core package that a voluntary offering could address at minimal employer cost?

The Employee Assistance Program: The Most Overlooked Benefit in Most Packages

The EAP is typically one of the lowest-cost benefits in any package and one of the most consistently underutilized. Most EAPs provide employees and their household members with free, confidential access to mental health counseling sessions, financial coaching, legal consultations, and other support services. The value is real and the cost to the employer is minimal. The problem is that most employees either do not know the EAP exists or do not understand what it covers.

A great benefits package not only includes an EAP but communicates it proactively and normalizes its use. When employees feel comfortable reaching out before a situation becomes a crisis, the EAP delivers returns that extend well beyond the benefit itself.

Self-Assessment Questions for the EAP

☐ Do employees know our EAP exists and how to access it?

☐ Have we communicated what the EAP covers beyond just mental health counseling?

☐ Have we normalized EAP usage by talking about it as a general resource rather than a last resort?

Benefits Communication: The Multiplier That Most Employers Underestimate

Here is a truth that does not get enough attention: the quality of your benefits communication matters almost as much as the quality of your benefits. An excellent package that employees do not understand delivers far less value than a good package that employees know how to use.

Great benefits packages are supported by year-round communication, not just an annual open enrollment push. They use plain language that employees at every level can understand. They explain not just what is available but why it matters and how to actually use it. And they give employees a clear point of contact when they have questions.

If open enrollment is the only time your employees hear about their benefits, you are leaving a significant amount of the value you have paid for on the table.

Self-Assessment Questions for Benefits Communication

☐ Do we communicate about benefits more than once a year?

☐ Do employees know who to contact when they have a benefits question?

☐ Have we provided plain-language explanations of how our plans actually work?

☐ Do new employees receive a thorough benefits orientation within their first few days?

Bringing It Together: How Does Your Package Stack Up?

If you worked through the self-assessment questions above honestly, you should now have a clearer picture of where your benefits package is strong and where there are gaps worth addressing. A few patterns are worth noting.

If your gaps are primarily in communication, that is actually good news. Communication improvements tend to be low-cost and high-return, and they can produce meaningful improvements in employee satisfaction and utilization without requiring any changes to the underlying plan.

If your gaps are in specific benefit categories, such as an outdated dental maximum or inadequate disability coverage, those are targeted improvements that can often be addressed at renewal time without a significant increase in overall spend.

If your gaps are structural, meaning your health plan design, funding arrangement, or contribution strategy may not be right for your current workforce, those conversations take more time but are also the ones that tend to produce the most meaningful long-term results.

Whatever you found, the value of this kind of honest assessment is that it gives you a starting point for a better conversation with your benefits advisor. Rather than simply reacting to the next renewal, you are walking in with a clear view of what you are trying to accomplish and where your current package needs to go.

At Cypress Benefit Solutions, we work with employers of all sizes to evaluate their benefits packages honestly and build toward something that delivers real value for their employees and their business. If you would like to walk through your package together and identify where the best opportunities are, we would welcome that conversation. Reach out anytime.