On May 29, 2026, the IRS released the 2027 annual limits for health savings accounts, high deductible health plans, and excepted benefit health reimbursement arrangements through IRS Revenue Procedure 2026-24. The Department of Health and Human Services had previously issued the 2027 ACA out-of-pocket maximums in January. Together these updates give employers the full picture of what the key plan design numbers look like for the coming plan year.

For most employers these numbers land quietly in the middle of the year and get noticed, if at all, during open enrollment preparation. But understanding them now matters because several of the 2027 limits reflect meaningful increases from 2026 that have practical implications for plan design decisions, employee communication, and contribution strategy conversations that are best handled well before renewal season rather than during it.

This post walks through each category of limits, explains what the numbers mean in practice, and identifies the places where employers and HR leaders should be paying particular attention.

Health Savings Account Contribution Limits for 2027

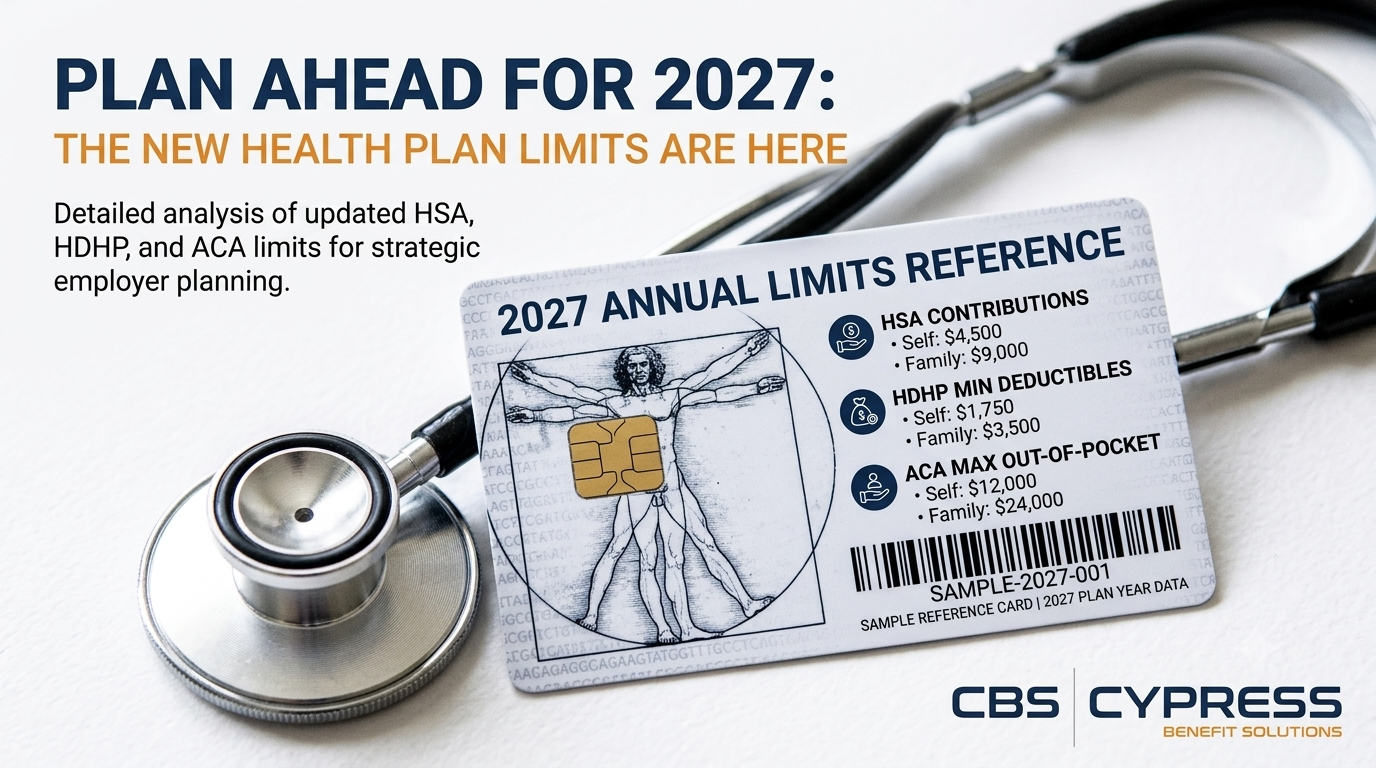

The IRS has increased the annual HSA contribution limits for 2027 for both self-only and family coverage. Here is a side-by-side look at where the limits stand:

Self-only coverage | $4,500 (up $100 from $4,400 in 2026)

Family coverage | $9,000 (up $250 from $8,750 in 2026)

Catch-up contribution (age 55 or older) | $1,000 (unchanged from 2026)

The increases are modest but meaningful for employees who are maximizing their HSA contributions each year. A family that contributes the maximum in 2027 will be putting aside $9,000 in pre-tax dollars for qualified medical expenses, which at a 22% federal income tax bracket represents roughly $1,980 in tax savings on contributions alone, not counting the tax-free growth and tax-free withdrawal benefits that make the HSA a uniquely powerful savings vehicle.

For employers, the HSA contribution limit increase is relevant in a few ways. Employers who make contributions to employee HSAs as part of their benefits strategy, whether as a flat dollar amount or as a match on employee contributions, should review whether their current contribution levels are still aligned with their goals relative to the new maximum. Employers who have not previously offered an employer HSA contribution may find that the increasing limits make this a more attractive differentiator in their total compensation package.

It is also worth noting that the catch-up contribution limit for employees age 55 and older remains at $1,000, unchanged from prior years. Older employees who are eligible for catch-up contributions can put aside a total of $5,500 for self-only coverage or $10,000 for family coverage in 2027.

High Deductible Health Plan Minimums and Maximums for 2027

To be eligible to contribute to an HSA, an employee must be enrolled in a qualifying high deductible health plan. The IRS defines HDHPs by both a minimum deductible threshold and a maximum out-of-pocket limit. For 2027 both of those thresholds have increased:

Minimum Annual HDHP Deductible

Self-only coverage | $1,750 (up $50 from $1,700 in 2026)

Family coverage | $3,500 (up $100 from $3,400 in 2026)

Maximum Annual HDHP Out-of-Pocket Expenses

Self-only coverage | $8,700 (up $200 from $8,500 in 2026)

Family coverage | $17,400 (up $400 from $17,000 in 2026)

These numbers define the boundaries within which a plan must fall in order to qualify as an HDHP and preserve employee HSA eligibility. For employers whose plan designs are currently close to the minimum deductible thresholds, the 2027 increases are relevant because a plan that met the minimum deductible threshold for 2026 may no longer qualify as an HDHP in 2027 if the deductible has not also increased accordingly.

This is a point worth reviewing carefully with your benefits advisor before the 2027 plan year begins. An employer whose HDHP deductible sits at exactly the 2026 minimum of $1,700 for self-only coverage will need to adjust it to at least $1,750 to maintain HDHP status in 2027, otherwise employees enrolled in that plan would lose their HSA eligibility. That is a compliance issue that is easy to miss and important to catch before open enrollment communications go out.

The maximum out-of-pocket increases also matter from a plan design standpoint. The HDHP out-of-pocket maximum caps the total exposure an employee can face in a plan year under a qualifying HDHP. Employers who are designing or adjusting their HDHP plan design for 2027 have somewhat more room to set the out-of-pocket maximum before running into the IRS ceiling.

ACA Out-of-Pocket Maximum Limits for 2027

Separate from the HDHP out-of-pocket maximums described above, the ACA establishes its own out-of-pocket maximum limits that apply to non-grandfathered health plans. For plan years beginning in 2027 those limits are:

Self-only coverage | $12,000 (up $1,400 from $10,600 in 2026)

Family coverage | $24,000 (up $2,800 from $21,200 in 2026)

The increases here are notably larger than in prior years, driven by the methodology the Department of Health and Human Services uses to adjust these limits annually. A $1,400 increase in the self-only limit and a $2,800 increase in the family limit represent a significant jump that has practical implications for both employers and employees.

It is important to understand what the ACA out-of-pocket maximum actually covers. Unlike the HDHP out-of-pocket maximum, which applies to all covered services under the plan, the ACA out-of-pocket maximum applies specifically to in-network essential health benefits for non-grandfathered plans. Cost sharing for out-of-network services and non-EHB services may be subject to separate limits or no limit at all depending on plan design.

For employers, the increase in the ACA out-of-pocket maximum means that plan designs that were already at or close to the prior year limit now have more room to set the out-of-pocket maximum before hitting the ceiling. This does not mean employers should automatically increase employee cost exposure to match the new limit, but it is useful context for plan design conversations at renewal.

For employees, the increase means that the theoretical maximum out-of-pocket exposure for in-network essential health benefits has grown. This is particularly relevant for employees on high-deductible plans who may be relying on the ACA limit as a backstop against catastrophic cost exposure. Employers should make sure their employee communications for the 2027 plan year clearly explain what the out-of-pocket maximum covers and what it does not.

Excepted Benefit HRA Limit for 2027

The annual maximum for excepted benefit health reimbursement arrangements for 2027 is $2,250. Excepted benefit HRAs are employer-funded accounts that can be offered alongside traditional group health plan coverage to reimburse employees for certain qualified excepted benefits, such as dental and vision expenses, regardless of whether the employee is enrolled in the main group health plan.

Unlike HSAs or FSAs, excepted benefit HRAs are funded entirely by the employer. They are a relatively flexible tool for employers who want to provide additional reimbursement support for benefits that fall outside the main health plan without the complexity of an ICHRA or QSEHRA structure. The $2,250 limit for 2027 reflects the maximum annual amount an employer can make available through this type of arrangement.

Why These Numbers Matter Before Renewal Season

The 2027 limits are released in May and June for a reason: plan years beginning January 1, 2027 are not that far away, and the decisions that shape those plans are made during the fall renewal and open enrollment cycle. Employers who understand the new limits now have several months to incorporate them into their planning conversations, update their contribution strategies, review their plan designs for compliance, and prepare employee communications that reflect accurate numbers.

Employers who wait until renewal pressure arrives to review these numbers end up making faster, less considered decisions. Those who engage with them now tend to show up to renewal conversations better prepared, with more options and a clearer sense of what they are trying to accomplish.

A few specific action items worth putting on the calendar before fall:

- Confirm that any HDHP plan design your company offers still meets the 2027 minimum deductible thresholds to preserve employee HSA eligibility

- Review your employer HSA contribution strategy in light of the new maximums and consider whether adjustments are warranted

- Update any employee-facing materials that reference current year limits so they are accurate for the 2027 plan year

- Review your plan’s out-of-pocket maximum structure in light of both the HDHP and ACA limit changes and discuss with your advisor whether any plan design adjustments are appropriate

- Communicate the new HSA contribution limits to employees early so those who want to maximize contributions can plan their paycheck deductions accordingly

How Cypress Benefit Solutions Can Help

Staying current on annual limit changes and understanding their practical implications for plan design, employee communication, and compliance is exactly the kind of year-round advisory work that separates a strategic benefits partner from a broker who shows up at renewal time with a quote.

At Cypress Benefit Solutions, we monitor regulatory and IRS updates like these as they are released and help our employer clients understand what they mean before they become a problem. If you have questions about how the 2027 limits affect your specific plan design, your HSA contribution strategy, or your employee communications, we would be glad to work through it together. Reach out anytime.